How do you build trust?

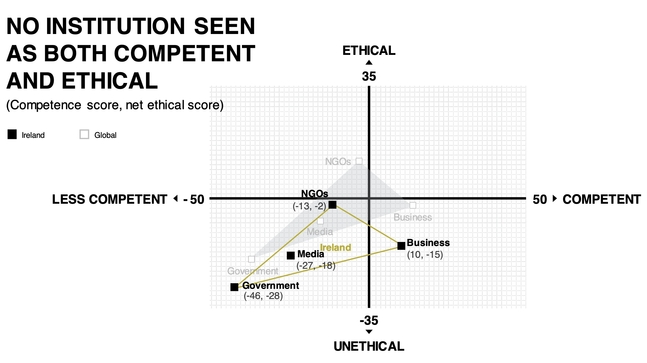

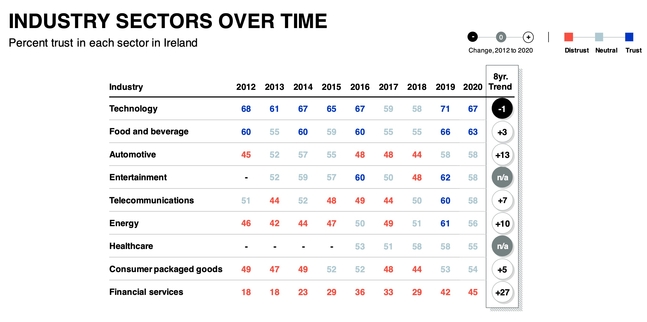

I recently shared the most relevant findings for financial advisers in the Edelman Trust Barometer 2020, in which we saw continuing challenges for the financial services industry in relation to trust. However we also saw that trust in the financial services industry is growing faster than any other sector, so the graph is definitely moving in the right direction!

I got a lot of feedback in relation to this article, thanks for all your likes and comments – much appreciated as ever. A few advisers have since asked me what they need to do in order to build trust. So here goes – my thoughts on a few ways that really help to build trust.

Be visible when the going gets tough

This is so relevant today, with the Covid-19 pandemic and investment markets crashing to the floor. Now is not the time to go to ground and hope that clients won’t ring about their falling investments. Instead now is the time to be calm, show your leadership qualities to clients and remind them that their financial plan will deliver the desired outcomes over time. Yes, acknowledge the discomfort caused by markets today, but remind clients that this will pass. Your visibility and reassurance will provide comfort to clients, and will help build their trust in you.

Communicate how you work with clients

One of the most important ways to build trust, particularly with potential clients, is by communicating really clearly how you will actually work with them. Many people only sort of know what a financial adviser does – something to do with pensions and life assurance? Let potential clients know the problems you solve and the outcomes you achieve for them. And then explain how you will work with them. You can give huge levels of comfort by walking the client through your advice process in detail, showing them what to expect and the value that you will add. This will help to remove any doubts in their mind.

Provide client testimonials

Continually seek out client testimonials, they are really important. In my book, you need to seek permission to use the client’s actual name (and logo if a company). Testimonials from “John H, Dublin” don’t really count – in fact someone might suspect they are made up! Genuine client testimonials are really powerful – who can advocate for you better than people who you’ve helped in the past, whose lives you have potentially changed?

Seek recommendations on LinkedIn

LinkedIn is a really important platform for financial advisers; it’s where many prospective clients will check you out before picking up the phone to you. After all, when they Google your name, the chances are that your LinkedIn profile will appear high up the search results. Recommendations from clients on your LinkedIn profile are a very powerful endorsement of your services, so look for these at every opportunity. They are great trust builders.

Presence in mainstream press

Some advisers have built up great profiles by regularly appearing in “Opinion” columns in national newspapers and some even building positions as regular commentators on TV and radio. These are great for building trust, as they demonstrate your industry knowledge and authenticity as a voice worth listening too.

Your qualifications

Sounds simple? If I was a CFP, I’d tell everyone at every opportunity! Why not advertise the fact that you are part of a highly qualified cohort? Prospective clients will value the fact that you are investing in yourself and are willing to keep learning in order to stay at the frontier of providing the very best financial advice. It will also help you to achieve high levels of trust among clients.

There are of course many more ways of building trust; advertising any awards that you win, communicating your opinions with your clients via newsletters and being active on social media. Hopefully the ideas above will give you a few pointers as to how you can continue to build trust with your clients and prospective clients.